What happened in Q1 of 2025

Q1 saw stabilizing market activity early, but finishing muddy and slow due to Buyers pausing in reaction to tariff and stock market concerns. Jan and Feb started extremely well outpacing 2024’s start and sending clear signals that market had indeed bottomed in Q4 2024 with 17% jump in pendings, and all price bands showing great market activity compared to last few years.

However in March, once tariff talks started and the stock market slide happened, Buyer decisions became sticky and stretched over time. Decisions were taking double the time.

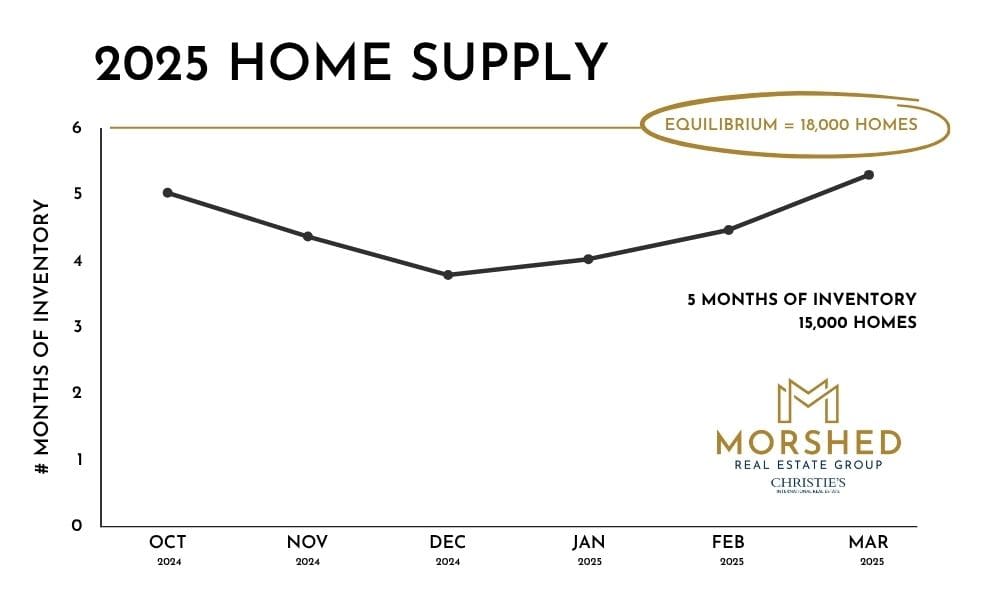

While Jan and Feb saw supply banding down to 4.5 months, after March we saw a jump to 5.5 months which equates to 3k more homes on the market

For context, a 6-month supply (or about 18,000 homes available) is an equilibrium market between Buyer and Seller demand and we would normally see 4-6% annually in price rises. At 5 months supply, there are about 14k homes on the market.

However, we believe that this is temporary vs another big pullback on values in Austin’s market. Why? Prices held steady through Q1 even though supply jumped marking 3 consecutive quarters where values didn’t drop more than 1%. This is a strong indicator. Two, mortgage applications locally actually moved up in Q1 in spite of rates still being 6.5%+. It’s a clear indication “normalizing” is happening around rates for consumers. Additionally, the local job market didn’t react with layoffs, another good sign. Unemployment still held at 3.5%, great numbers.

Currently and where it’s going

Q2 has seen the market bump along the same way as I just mentioned. Stock market and tariff concerns have tempered for now, but Buyers are skittish till there is further clarity on economic policy. This is is especially showing up in the higher end.

All being said, Buyer activity and traffic are just as high through January which is notable. This signals the Buyers are there and active, and once there is clarity, we fully expect the market to get back to the clearly more robust activity of Jan through early March. We still see 2025 as a year that the market stabilizes. However where there was a possibility of slight appreciation towards Q4, it’s likely zero oat this point.

For Sellers

For Sellers, 2025 has started better. While temporarily it’s sluggish, there is no question there is more traffic in the market. Hang in there. Buyers will start transacting with more confidence 3-6 months out and you’re still better off selling now vs last year. You’ll still have to negotiate to sell still but on average 5% or less from your market value, a marked improvement.

For Buyers

For Buyers, we still believe this is the bottom. Buy now and this year. When there is confidence/clarity around tariffs it’ll mean less negotiability for you. Buy now so you can pick up 6-8% appreciation starting next year depending on area.